本文作者系上海邦信阳中建中汇律师事务所合伙人刘倩律师、 王萍律师。

2015年9月21日,我国国务院副总理马凯和英国财政大臣奥斯本共同主持了第七次中英经济财金对话。中英双方在此次财金对话中就宏观经济形势和政策、贸易投资、金融监管、发展和合作达成了众多共识,其中在资本市场合作方面,双方均表示“支持上海证券交易所与伦敦证券交易所就互联互通问题开展可行性研究”,即:“沪伦通”将进入可行性研究阶段。

伦敦证券交易所是全球四大证券交易所之一,伦敦作为世界上最国际化的金融中心,不仅是欧洲债券及外汇交易领域的全球领先者,还受理超过三分之二的国际股票承销业务。此次“沪伦通”的提出,将加速国内资本市场的国际化以及中国资本账户的对外开放。

目前“沪伦通”仅是一个概念设想,尚未成形,基于“沪港通”的运行模式,结合伦敦证券交易所的自身特点,笔者对“沪伦通”猜测如下:

可能借鉴“沪港通”的部分

“沪港通”在遵循两地现行的交易结算、业务及监管规则的基础上,建立了沪港股票市场交易互联互通机制,未来“沪伦通”的架构搭建和可行性研究亦不会违背内地和伦敦两地市场现行的交易、结算、业务及监管规定,“沪伦通”将求同存异,寻求双方股票市场互联互通的平衡点。

“沪港通”是指,上海证券交易所和香港联合交易所有限公司建立技术连接,使内地和香港投资者通过当地证券公司或经纪商买卖规定范围内的对方交易所上市的股票。

“沪港通”包括沪股通和港股通两部分,沪股通系香港投资者可参与买卖的规定范围内的上海证券交易所上市的股票,港股通系内地投资者可参与买卖的规定范围内的相关联合交易所上市的股票。沪股通的总额度为人民币3000亿元、每日限额为人民币130亿元;港股通的总额度为人民币2500亿元、每日限额为人民币105亿元。截止至2015年10月23日,沪股通剩余额度为人民币1577.55亿元,占总额度的52.59%;港股通剩余额度为人民币1608亿元,占总额度的64.32%。由此可以看出,香港投资者对于内地资本市场的投资热情更高,内地资本市场虽然近期波动较大,但对投资者仍具有吸引力。

笔者认为“沪伦通”可能借鉴“沪港通”的内容如下:

(一)双方均会规定被纳入“沪伦通”交易的股票范围;

(二)在对方所在地设立证券交易服务公司;

(三)由各自的登记结算公司办理登记、存管、结算服务;

(四)双方投资者通过当地证券公司或经纪商购买对方交易所上市的股票;

(五)中国登记结算公司和伦敦登记结算公司作为双方投资者所购买股票的名义持有人,根据投资者的要求进行股票交易;

(六)中国对境外投资者的境内股票投资的持股比例予以一定的限制;

(七)对参与“沪伦通”的内地个人投资者设置一定的要求。

待突破的部分

1.时差

上海与伦敦分处不同的时区,上海闭市的时间,恰是伦敦开市时间,这将致使“沪伦通”如何进行清算和结算成为最大的问题。目前,“沪港通”选择两地市场的共同且能够同时满足结算安排的为交易日,故“沪伦通”如何解决时差带来的问题,需待中英双方进行探讨和研究。

2.结算货币

“沪港通”以人民币作为投资者与证券公司或经纪商进行交收的唯一货币。在“沪伦通”中,若以人民币作为唯一的结算货币,鉴于伦敦证券交易所股票的挂牌价格系以英镑计算,对于汇率差异、货币兑换等的处理,亦将成为中英双方研究“沪伦通”可行性的重点。

3.风险防范及市场监管

鉴于,伦敦证券交易所与上海证券交易所无论是交易规则、监管制度、市场基础设施等都存在着较大的差异,例如:伦敦证券交易对于个股的涨跌幅没有限制、交易方式采用的是“T+0”的模式,且对于个股出现异常情况的(①SEAQ系统内,个股最佳买进或卖出申报价格涨跌幅超过其基准价格的5%;②SETS系统内,个股涨跌幅超过前一笔成交价格5%时),伦敦交易所将采取个股交易暂停5分钟的措施。

如何在不改变双方现行交易机制的前提下,兼顾风险控制和双边不同交易制度,保证双边市场的稳定性、保障投资者的合法权益,以及“沪伦通”开通后的,跨境执法和市场监管,都将有待中英双方突破和创新。毕竟,“沪伦通”有别于“沪港通”,“沪伦通”不可能简单复制“沪港通”的模式,势必会在“沪港通”的基础上,结合中英的实际情况,进行探索、研究和创新,从而挖掘出“沪伦通”的可行性、科学性。

交易规则

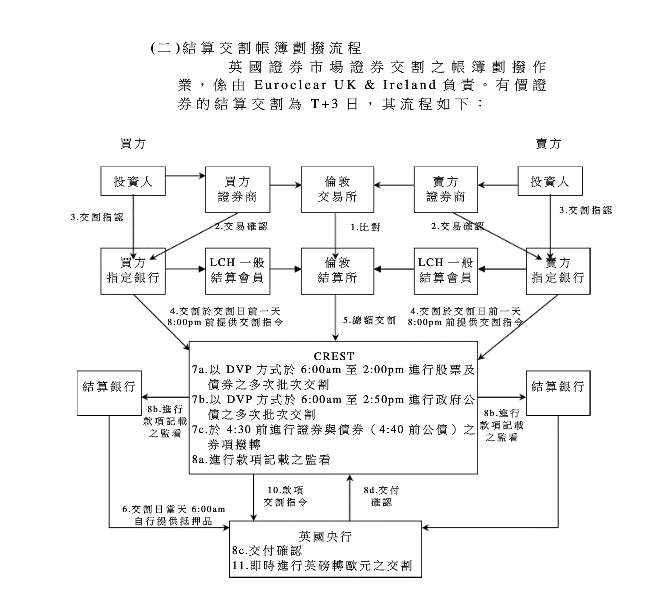

1. 交易结算流程

(1)伦敦证券交易所有价证券交易结算流程

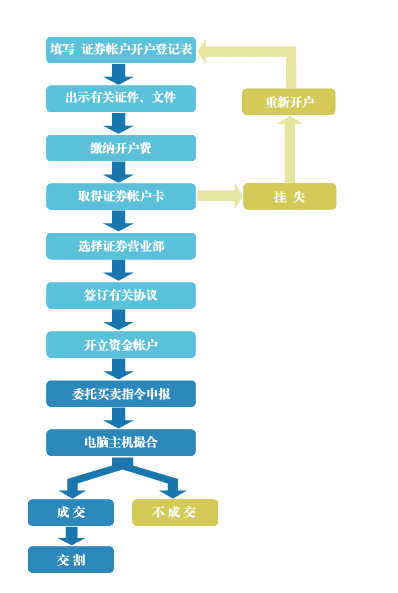

(2)上海证券交易所交易流程

笔者认为,“沪伦通”开通后,根据伦敦证券交易所和上海证券交易所现行的交易流程,以及“沪港通”的交易模式,双方投资者通过当地证券公司或经纪商购买对方交易所上市的股票,所买入的股票将分别登记在中国登记结算公司和伦敦登记结算公司名下,由登记结算公司名义持有,出具股票持有记录作为投资者享有股票权益的证明。

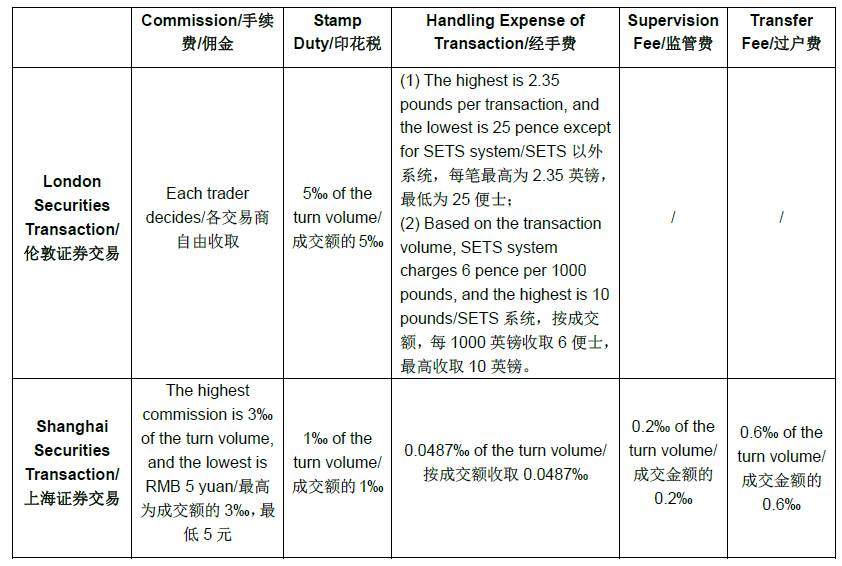

2. 交易成本

以上,是笔者基于现行“沪港通”的相关机制,对未来“沪伦通”可能的发展方向所做的推测,以及对上海证券交易与伦敦证券交易所在交易流程和交易成本上所做的简要对比。

随着人民币国际化进程的加速,“沪伦通”已进入可行性研究阶段,未来可能还会开启“沪纽通”等对接国外发达资本市场的通道。“沪伦通”的可行性研究,极有可能成为“沪纽通”等的创新基础。笔者亦将积极关注“沪伦通”的推进情况,并分享相关进展。

On September 21, 2015, Chinese Vice-Premier Ma Kai and UK’s Chancellor of the Exchequer George Osborne concluded the 7th China-UK Economic and Financial Dialogue. The Vice-Premier and Chancellor agreed a number of outcomes regarding macroeconomic situation and policies, trade and investment,financial regulation, development and cooperation. In the capital market cooperation, China and UK both support the Shanghai Stock Exchange (“SSE”) and the London Stock Exchange Group (“LSEG”) to carry out feasibility study on a stock connect, which means the Shanghai-London Stock Interconnection comes into feasibility study.

LSEG is one of the four big stock exchanges in the world, and London, as the most international financial center, not only is the global leader in the field of European bonds and foreign exchange trade, but also accepts more than two-third international equity underwriting business. The Shanghai-London Stock Interconnection will accelerate the internationalization of domestic capital market and Chinese capital account opening-up.

Currently the Shanghai-London Stock Interconnection is just a concept, not be formed. Based on the operation mode of the Shanghai-Hong Kong Stock Interconnection, we conjecture the Shanghai-London Stock Interconnection as below:

System may refer to the Shanghai-Hong Kong Stock Interconnection

The Shanghai-Hong Kong Stock Interconnection establishes an interconnection mechanism in the Shanghai and Hong Kong stock markets based on complying with bilateral current transaction, settlement, business and regulatory rules. The Shanghai-London Stock Interconnection may seek the common ground while putting aside difference, finding balance of stock interconnection between both stock markets.

The Shanghai-Hong Kong Stock Interconnection means SSE and the Stock Exchange of Hong Kong Limited (“SEHK”) establish technical connection to allow mainland and Hong Kong investors to trade in a specified scope stocks listed on the other through local securities companies or brokers.

The Shanghai-Hong Kong Stock Interconnection consists of a northbound trading link (“NTL”) and a southbound trading link (“STL”). Under the NTL, investors from Hong Kong may trade in a specified scope stocks listed on the SSE. Under the STL, investors from the mainland may trade in a specified scope stocks listed on SEHK. The total amount of NTL is RMB 300 billion, and the upper limit of NTL per day is RMB 13 billion; the total amount of STL is RMB 250 billion, and the upper limit of STL per day is RMB 10.5 billion. Till October 23, 2015, the balance of NTL is RMB 157.755 billion, accounting for 52.59% of the total amount; and the balance of STL is RMB 160.8 billion, accounting for 64.32% of the total amount, which indicates that the Hong Kong investors show higher enthusiasm for investment in mainland capital market, and mainland capital market is still attractive to the investors although it fluctuated widely recently.

The content of Shanghai-London Stock Interconnection may refer to Shanghai-Hong Kong Stock Interconnection as below:

(1) Both parties will prescribe a stock scope of Shanghai-London Stock Interconnection;

(2) Establishing securities trading service company on the other side;

(3) Each depository and clearing company proceeds its registration, depository and clearing service;

(4) Both investors trade stocks listed on the other stock exchange through local securities companies or brokers;

(5) Both depository and clearing companies as the nominee holder of the stock purchased by the local investors trade the stock as investors required;

(6) China may set limitation to the foreign investors holding the shares of the local stock investment;

(7) Setting certain requirements for mainland individual investors participating in Shanghai-London Stock Interconnection.

System to be broken

I. Time Difference

Shanghai and London are at different time zone. The market closing time in Shanghai is just the market opening time in London, which will make clearing and settlement to be the biggest problem of the Shanghai-London Stock Interconnection. Currently Shanghai-Hong Kong Stock Interconnection selects the day which is the trading day in both sides and may meets the settlement arrangement simultaneously as the trading day, so how to solve the problems arising from time difference needs China and UK to discuss and study.

II. Settlement Currency

RMB, as the only currency, is used to delivery with securities companies or brokers by investors. If RMB is the only settlement currency in Shanghai-London Stock Interconnection, as the listing price on LSEG is pound, how to handle the difference in exchange rates, currency swap, etc. will be key points of the feasibility study between China and UK.

III. Risk Prevention and Market Supervision

There is a big difference in transaction rules, regulatory systems, market infrastructure, etc. between LSEG and SSE, for example, the absence of price fluctuation restrictions of LSEG, “T+0” of the transaction method, and a five-minute transaction suspension of the individual stock taken by LSEG when it occurs abnormal situation (①The price fluctuation of best buying or selling declaration price of the individual stock is more than 5% of its benchmark price in SEAQ system; ② The price fluctuation of the individual stock is more than 5% of its previous transaction price in SETS system.).

How to focus on risk control and bilateral transaction rules, guarantee the stability of bilateral market, protect investors’ legal rights and interests, and conduct cross-border enforcement and market supervision after Shanghai-London Stock Interconnection launched will be broken and innovated by China and UK. After all, Shanghai-London Stock Interconnection is difference from Shanghai-Hong Kong Stock Interconnection, Shanghai-London Stock Interconnection may not simply copy from the mode of Shanghai-Hong Kong Stock Interconnection. China and UK may proceed explore, study and innovate to find the scientificity and feasibility of Shanghai-London Stock Interconnection based on the Shanghai-Hong Kong Stock Interconnection and China and UK actual situation.

Transaction Rules

I. Transaction and Settlement Procedures

i. LSEG Securities Transaction and Settlement Procedures

ii. SSE Transaction Procedures

II. Transaction Cost

Foresaid content is a conjecture regarding the possible development direction of future Shanghai-London Stock Interconnection based on current relevant provisions of Shanghai-Hong Kong Stock Interconnection, and a brief comparison of transaction procedures and costs between SSE and LSEG.

With the acceleration of the process of internationalization of RMB, Shanghai-London Stock Interconnection has entered into the stage of feasibility study, and the channel to foreign developed capital market, i.e. Shanghai-New York Stock Interconnection, may be launched in future. The feasibility study of Shanghai-London Stock Interconnection is likely to be the basis of innovation of Shanghai-New York Stock Interconnection, etc. We will pay close attention to the proceeding of Shanghai-London Stock Interconnection and share relevant progress.